Do renewables make electricity cheaper or more expensive?

The honest answer is: it depends on what you measure, and where you look.

There are two stories people tell about renewables and electricity prices. One says more wind and solar are driving bills up. The other says renewables are bringing bills down. I’ve been pulling together data on wholesale and retail prices across European countries and US states to see which story holds up. Neither one does, and the mess is where the interesting policy questions live.

Let me walk through what the data actually shows.

Wholesale prices: renewables help, gas dominates

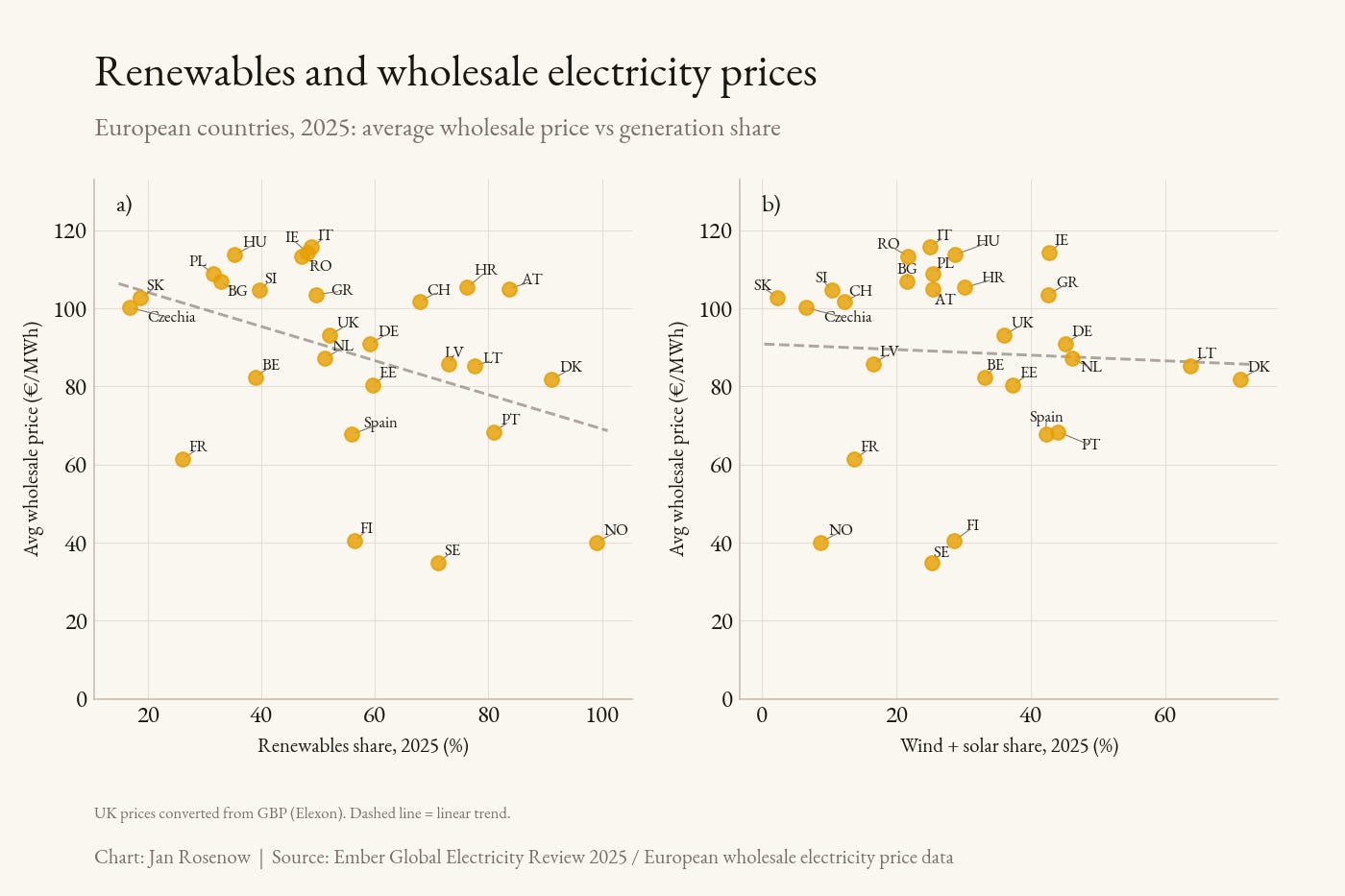

Start with European wholesale electricity prices in the first four months of 2026. Plot the average wholesale price against the total renewables share, country by country, and you see a negative slope. Countries with higher renewables shares tend to have lower wholesale prices. Spain and Portugal sit in the bottom right, with renewables shares above 60% and wholesale prices around €43/MWh. Slovakia, Czechia and Poland sit in the top left, with low renewables shares and prices above €100/MWh.

But strip out hydro and look only at wind and solar, and the relationship weakens. The slope flattens. Hydro-rich Norway and Sweden do a lot of the work in pulling the (weak) headline correlation down.

That doesn’t mean wind and solar fail to lower wholesale prices. The merit order effect is real and well-documented. It means that in any given year, wholesale prices reflect many things at once: gas exposure, hydro availability, weather, interconnection, market design. The renewables share alone doesn’t determine the price.

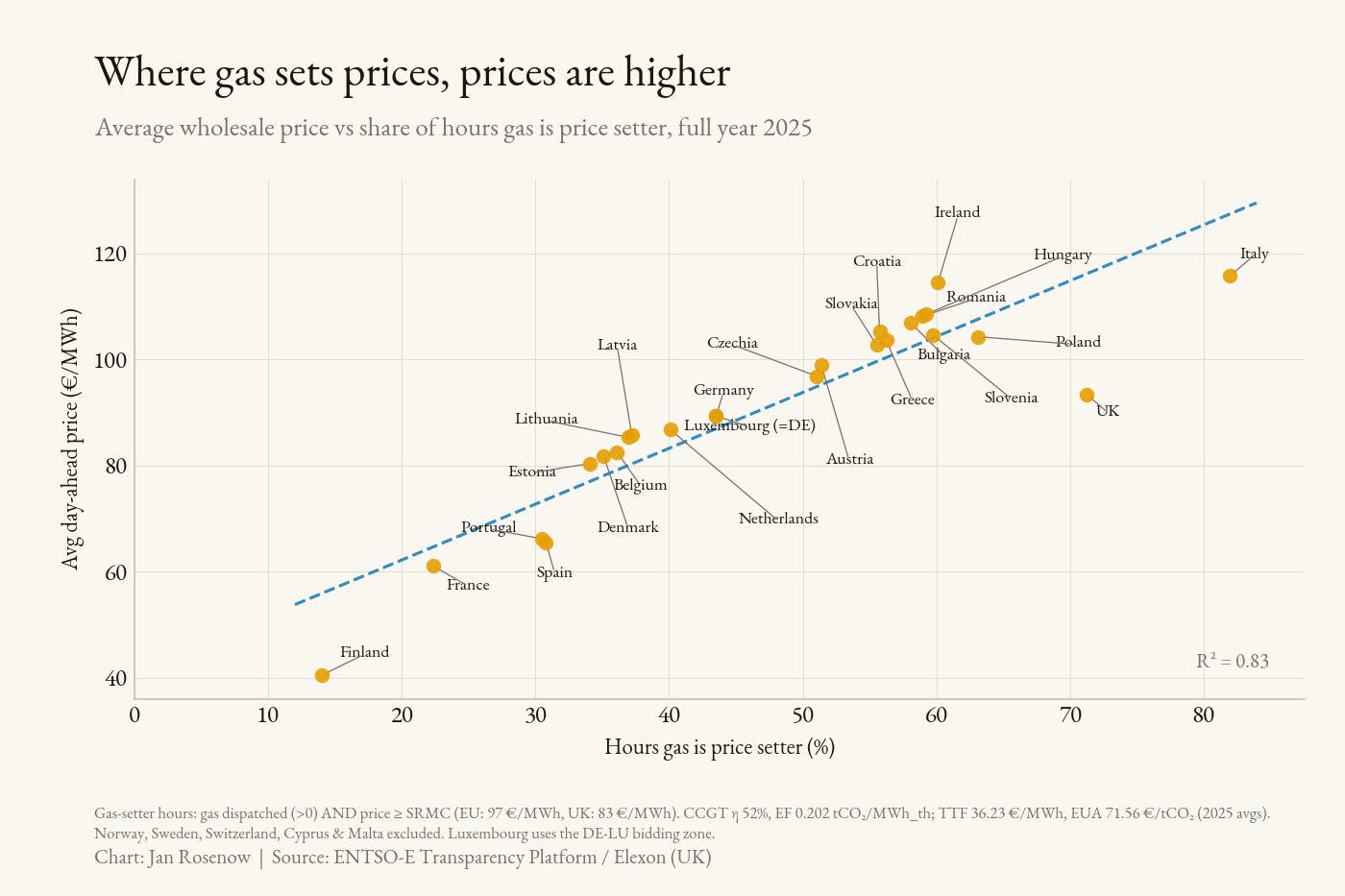

The single strongest predictor of wholesale prices in 2025 was something else entirely: the share of hours in which gas set the price.

Where gas sets prices, wholesale market prices are higher. That is the structural problem European electricity markets need to solve, and it is not a problem that the renewables debate, framed the way it usually is, addresses.

Gas sets the price less often when there is more non-fossil capacity available at the margin - renewables, storage, hydro, legacy nuclear, flexible demand, imports through interconnectors. The more physically and commercially connected markets are, the more often the marginal unit is something other than domestic gas.

The renewables share is part of that story, but so are the other pieces of the non-fossil system. Spain for example has low prices because it has solar, wind, hydro, and nuclear, and because storage and flexibility increasingly fill the gaps.

The country with the most renewables and nothing else is not the country with the lowest prices.

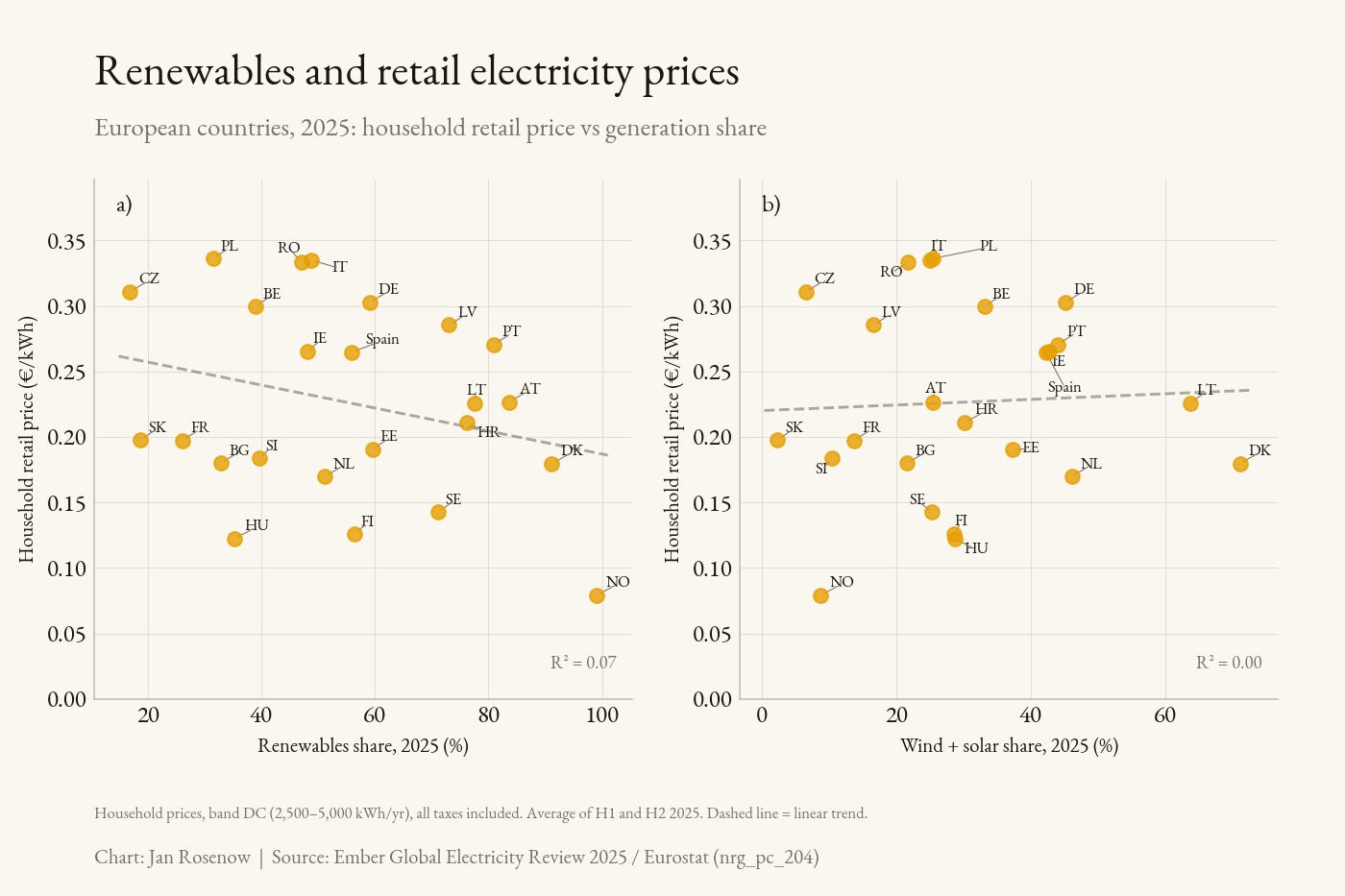

Retail prices: the link breaks down

Now look at retail prices, which is what households and businesses actually pay. Here the picture is more uncomfortable for clean energy advocates.

Across European countries in 2024 and 2025, household retail prices show essentially no relationship with the renewables share. The trend line is pretty flat. Portugal and Germany have similar renewables shares and very different retail prices. Norway has 99% renewables and the cheapest household electricity in Europe. Denmark has 91% renewables and prices well above the EU average. There is no clean pattern.

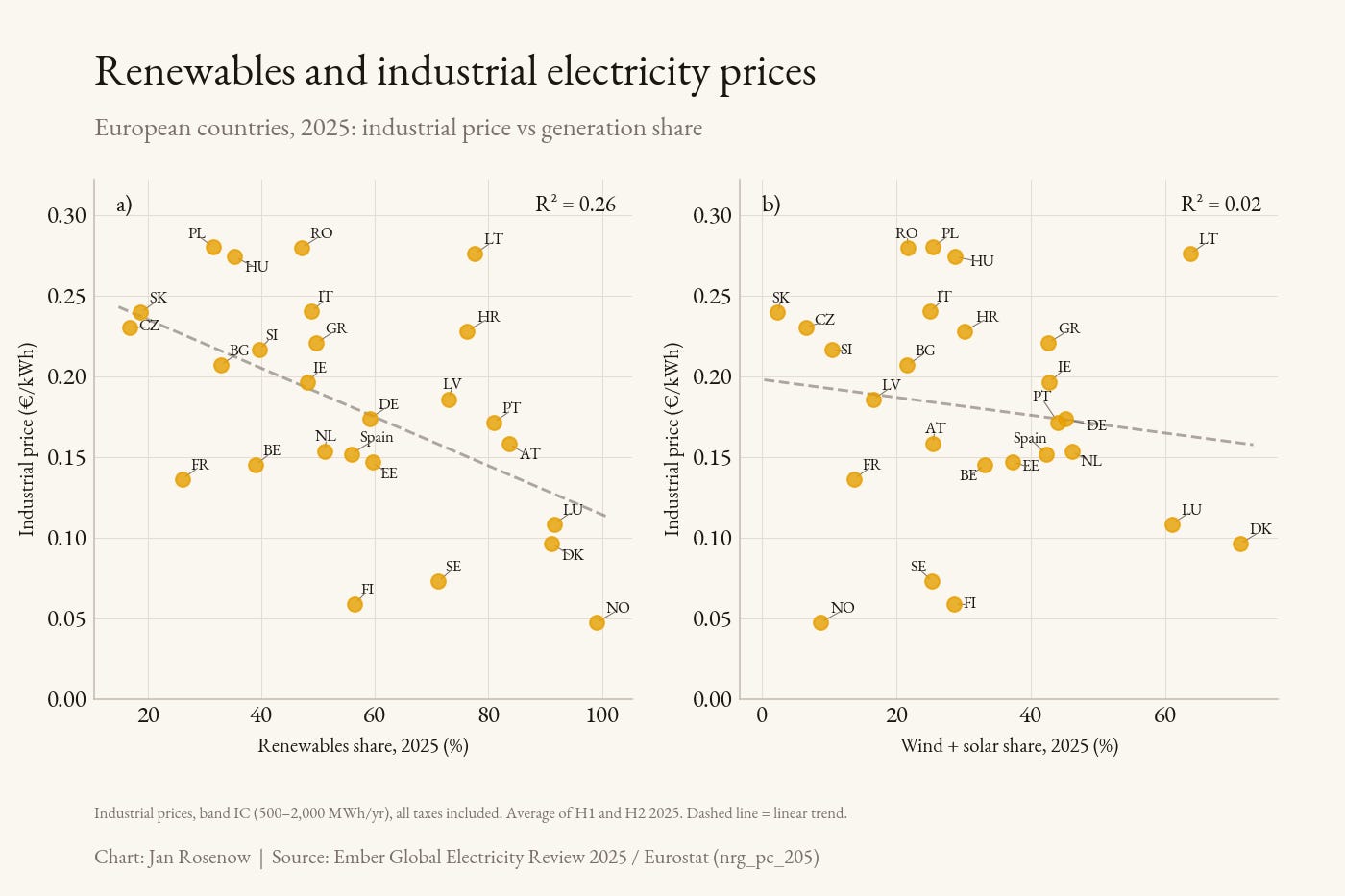

Industrial prices tell a slightly different story. Across European countries in 2025, the correlation between total renewables share and industrial electricity prices is meaningfully negative. Countries with more renewables in the mix pay less for industrial power. Norway, Denmark, Finland, Sweden and Luxembourg sit at the bottom. Poland, Romania, Lithuania and Italy sit at the top. But for wind+solar the relationship is very weak with no meaningful correlation.

The same is true across US states in 2024 and as Hannah Ritchie pointed out in her excellent article a while back: “Having lots of solar and wind doesn’t guarantee that you have cheaper or more expensive power than your neighbours. Nor does the absence of solar and wind guarantee that your power will be cheap.”

Wide variation in retail prices, a positive but fairly weak correlation with renewables share, and a slightly negative but also very weak correlation with wind and solar share. So renewables aren’t pushing retail prices up. But they aren’t pushing them down in any visible way either. But why?

The wedge between wholesale and retail

The reason is straightforward once you look at the components of a retail bill. Wholesale electricity is only part of what households and industry pay. Network charges, policy costs, taxes, levies and supplier margins make up most of the bill in many countries. These components don’t move with the wholesale price.

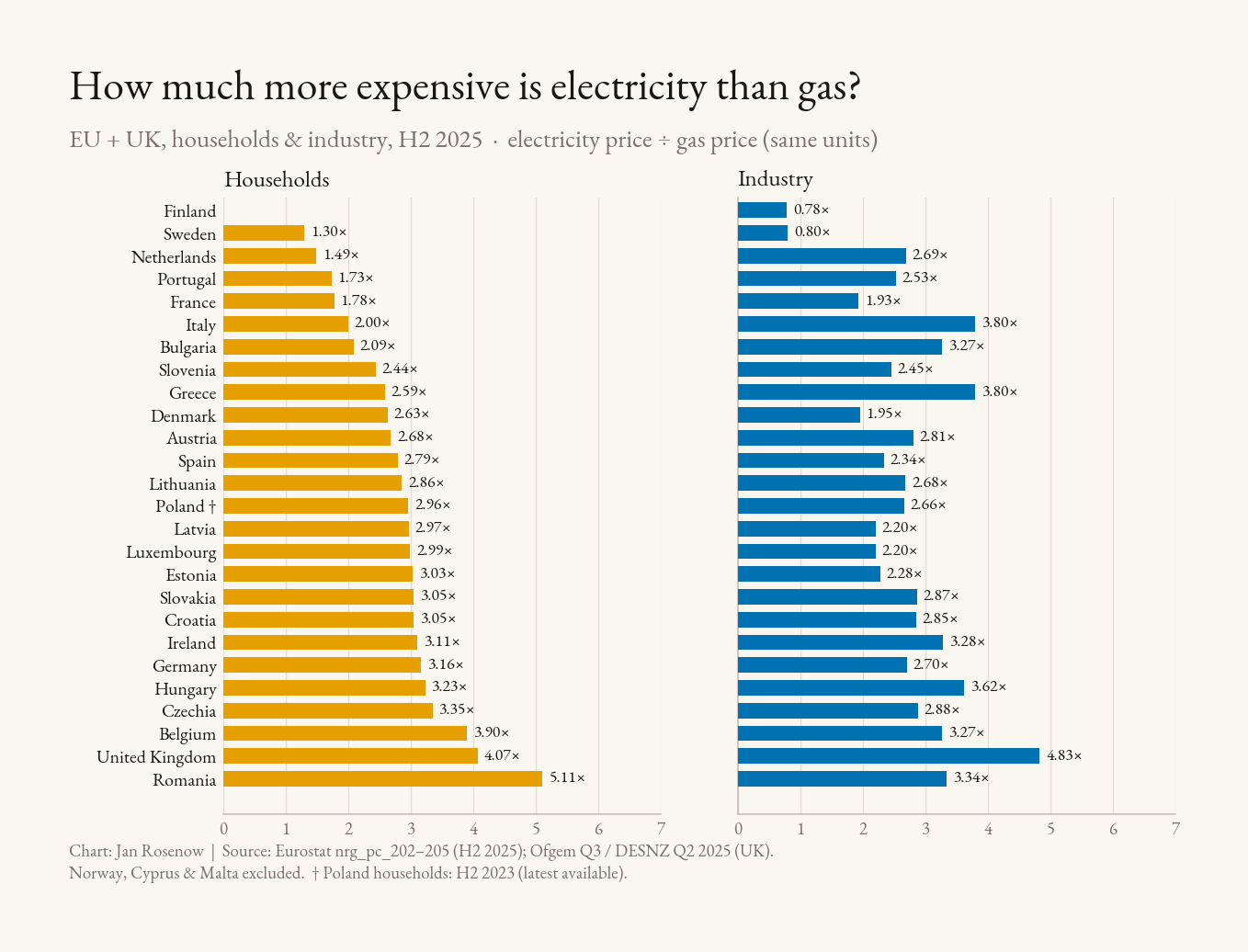

In many cases, the non-energy components of the electricity bill are responsible for unhelpfully large electricity to gas price ratios. In the second half of 2025, the average European household paid roughly 2.5 to 3 times more for a unit of electricity than for the same energy delivered as gas.

For industry, the spread is even wider. The UK industrial ratio is 4.83. Finland’s is 0.78, meaning industrial users actually pay less for electricity than for gas.

These ratios have very little to do with the cost of generating electricity. They have everything to do with how policy costs and levies are distributed across fuels. In most of Europe, electricity carries the bulk of the renewable energy and energy efficiency levies. Gas largely escapes them. The result is a price signal that actively discourages the electrification we say we want.

System costs: real, growing, and often misread

There’s a third element in the wedge that deserves its own paragraph: system costs. As wind and solar shares rise, so do the costs of integrating them. Curtailment when generation outruns what the grid can absorb. Balancing services to manage variability. Capacity mechanisms. Grid reinforcement to move electricity from where it’s generated to where it’s used. Research has long recognised these costs and produced estimates of how high these costs are.

These costs are real and they are growing. German curtailment compensation reached €2.8 billion in 2024. GB balancing costs have been running above £2 billion a year. In most countries they end up on the network charge line of the retail bill.

But two things are worth saying about them.

First, they are still a relatively small share of total system costs (here is more detail on the UK for example). They are not the dominant driver of retail prices. Levies, taxes and legacy network costs are usually bigger.

Second, they are partly a function of choices, not a fixed property of renewables. Curtailment is high where transmission build-out has lagged generation build-out, as it has in Germany and the UK. Balancing costs are high where flexibility markets are thin and interconnection is weak.

Countries that have invested in transmission, storage, demand-side flexibility and cross-border trade see lower integration costs at the same renewables share.

The “renewables make the system expensive” framing gets the causation backwards. It is the failure to build the rest of the system at the same pace required that drives the costs up.

This matters for the policy debate because system costs get used as a catch-all argument against further deployment. The honest answer is that they are real, they are manageable, and the way to keep them manageable is to build the grid and the flexibility and storage infrastructure that renewables need. Not to slow renewables.

What the data is telling us

Three things, I think.

First, the “renewables make electricity expensive” claim doesn’t survive contact with the wholesale data. Where renewables shares are high and gas exposure is low, wholesale prices are low. Spain, Portugal, France, Sweden and Norway all sit at the cheap end. The countries with the most expensive wholesale electricity are the ones still dependent on gas to set their prices. But consumers care about retail, not wholesale prices.

Second, the counter-claim that more renewables automatically delivers cheaper retail prices doesn’t survive either. The pass-through is broken. Households and businesses see their bills shaped far more by network charges, levies and tax design than by what is happening on the wholesale market.

Third, and this is the bit I find most important: the policy debate about electricity prices is the wrong debate if it stops at the wholesale market. The bigger lever, by far, is the structure of retail bills. Whether you load levies onto electricity or spread them across fuels. Whether you tax electricity at a higher rate than gas. Whether network charges are recovered through volumetric or capacity-based tariffs. These are choices, and they vary enormously across countries.

Norway, Sweden and Finland have built retail electricity markets where electrification makes economic sense for ordinary households and industry. Heat pump adoption tracks that. EV adoption tracks that. The technology is the same everywhere. The price signal is what differs.

If we want clean electricity to translate into clean heat, clean industry and clean transport, the wholesale market is doing most of its job. The retail market mostly isn’t. That’s the policy problem worth focusing on.

A reform agenda

So what would beneficial retail reform look like? Four things matter most. Rebalancing levies and taxes across fuels, so that gas carries its share of the policy and environmental costs rather than electricity carrying most of them. Letting temporal and locational price signals reach consumers, so that flexible demand can respond to what the system actually needs. Protecting vulnerable consumers through safety valve mechanisms and targeted support rather than through suppressed energy prices for everyone. And spreading the recovery of grid investment costs over a longer period, so that today’s bills do not have to carry the full cost of building the system tomorrow’s electrified economy will use.

Retail reform is not the only outstanding piece. Wholesale market design itself is still in motion: long-term contracts (PPAs and CfDs), supplier hedging, locational signals, demand-side access to balancing markets, cross-border infrastructure cost sharing. Getting those right will matter at least as much as fixing retail.

A harder question sits behind these: how much of this can competitive retail markets deliver, and how much needs the regulator or government to step back in? Across Europe the political momentum is towards a stronger public role. Whether that is the right direction is genuinely contested in the industry. What is not contested is that the current retail structure in most countries is not fit for an electrified system.

Where prices are heading

So what happens next? Three structural forces are now pushing in the same direction, and a fourth could undo a lot of the gains if policymakers get it wrong.

The first force is the steady decline in gas-setter hours. Spain is the clearest example. In 2024, gas set the wholesale price for roughly half of all hours. By early 2026, that share had fallen below 20%. Wholesale prices fell with it. The same pattern is starting to appear in other markets with high renewables shares. As wind and solar capacity grows and storage builds out, gas spends fewer hours at the margin. The mechanical link between European wholesale prices and the TTF gas price weakens. This is not a forecast. It is already happening in the countries furthest along.

The second force is generation cost. Solar PV is now the cheapest source of new electricity in most of the world. Onshore wind is close behind. Battery storage costs have fallen by roughly 90% in the last decade. New-build renewables plus storage are now cheaper than running many existing gas plants in much of Europe. And the cost curve has not bottomed out.

The levelised cost of energy (LCOE) metric on its own understates this, because it ignores when electricity is produced and what it is worth at that moment. The IEA’s value-adjusted LCOE, or VALCOE, captures that better. It adjusts the headline cost for the energy, capacity and flexibility value each technology actually delivers to the system. On that metric, solar and wind in most markets are not just the cheapest new build. They are the most valuable new build, even after accounting for the integration costs of variable generation.

The third force is the one people forget. Network charges, policy costs and grid investment are largely fixed in the short run. They are recovered by spreading the total bill across the kWh sold. If electricity demand grows, the same fixed costs are spread across more units. The per-kWh charge falls. This is the simple arithmetic of electrification. Heat pumps, EVs and industrial electrification all push electricity demand up. As they do, the network and policy components of the bill get diluted. A grid that delivers twice as much electricity does not cost twice as much to run. Electrification is, in this sense, its own affordability strategy.

Put these three forces together and the wholesale and underlying cost outlook is clear. Average wholesale prices fall as renewables are being added and replace gas. Volatility falls as storage and flexibility are scaled. The gas exposure that has dominated European electricity bills since 2021 fades. Fixed system costs get spread across a larger base. None of this is automatic, and the pace varies by country, but the direction of travel is not in doubt.

The fourth force is the one to focus on. Decarbonising the system requires major grid investment. Transmission build-out, distribution reinforcement, flexibility services and capacity mechanisms all cost money. Those costs land on the network charge component of retail bills. If electrification stalls, those costs get spread across a shrinking volume of electricity sales, and the per-kWh charge rises. The risk is a vicious circle: high retail prices discourage electrification, low electrification volumes drive up per-kWh network charges, higher charges discourage electrification further. Some of that is already visible in UK and German bills.

This is why retail reform matters more than it gets credit for. Ensuring that electricity is not excessively taxed compared to other energy vectors, and recovering costs in a way that supports dynamic efficiency and keeps cost down are the key ingredients. The countries that get this right will see lower wholesale prices feed through into lower bills, growing electrification volumes spreading fixed costs across more kWh, and stronger incentives for the next round of investment. The countries that don’t will see falling generation costs offset by rising network and policy costs, and households and businesses will conclude that the energy transition is making them poorer. Same underlying physics, opposite political outcomes.

The good news is that the bright spots are real. Wholesale markets are decoupling from gas. Electrification creates its own tailwind once it gets going. The harder question is whether retail markets will be redesigned fast enough to let the gains through.

Acknowledgements: I want to thank Bram Claeys from CEER for his helpful review and commentary on an earlier draft. Any errors remain mine and mine alone.